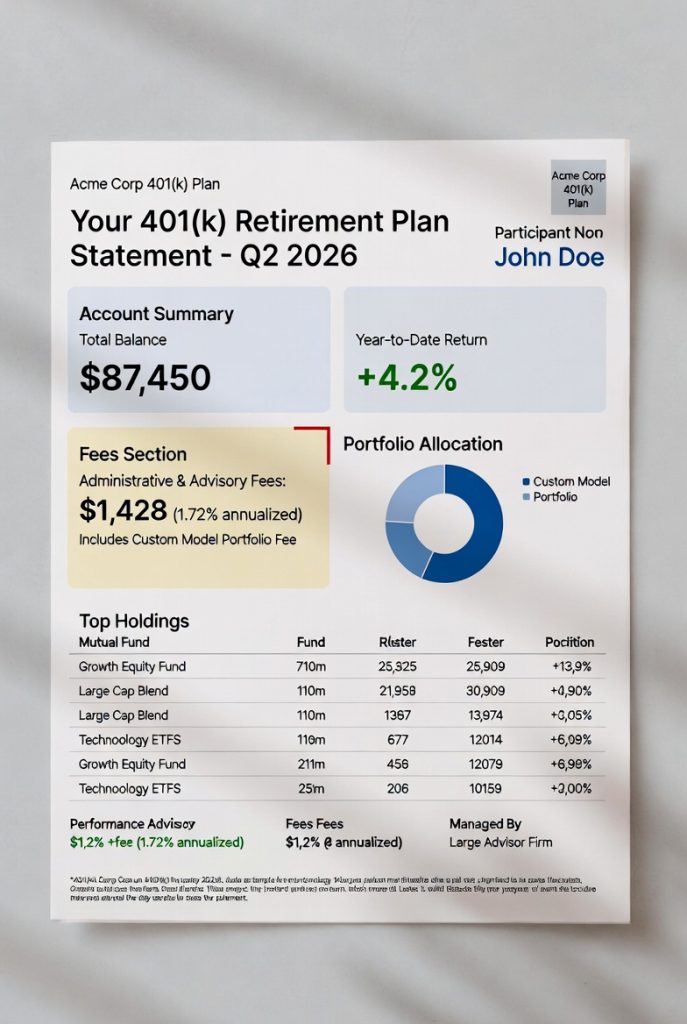

Financial Advisors, Financial Planners, and even things like 401(k) Plans offer “Model Portfolios.” The critical two questions that must be asked before anyone allows their hard earned money to flow into this type of investment are 1) what does it cost you? and 2) what do you get in return?

The image below is very typical of advisor groups offering to add custom model portfolios to workplace retirement plans. Custom Models (sometimes called “Managed Models”) are an add-on service to 401(k) Plans that are growing in popularity. Not all are bad, but some certainly are. This is where a little research comes in handy. The advisors behind the offering examined below list fees ranging from 1.56% to 1.85% – that’s a LOT OF MONEY!

Let’s put that fee into perspective: if your company 401(k) Plan has $10 million in it, these advisors might subtract around $185,000 in fees out of your and your co-workers’ accounts every year. In exchange for letting them siphon money out of your account, they’ll decide which mutual funds to put your money into, so you don’t have to.

This offering is VERY high cost; are you at least getting sound investment advice out of it? We’ll let you be the judge of that.

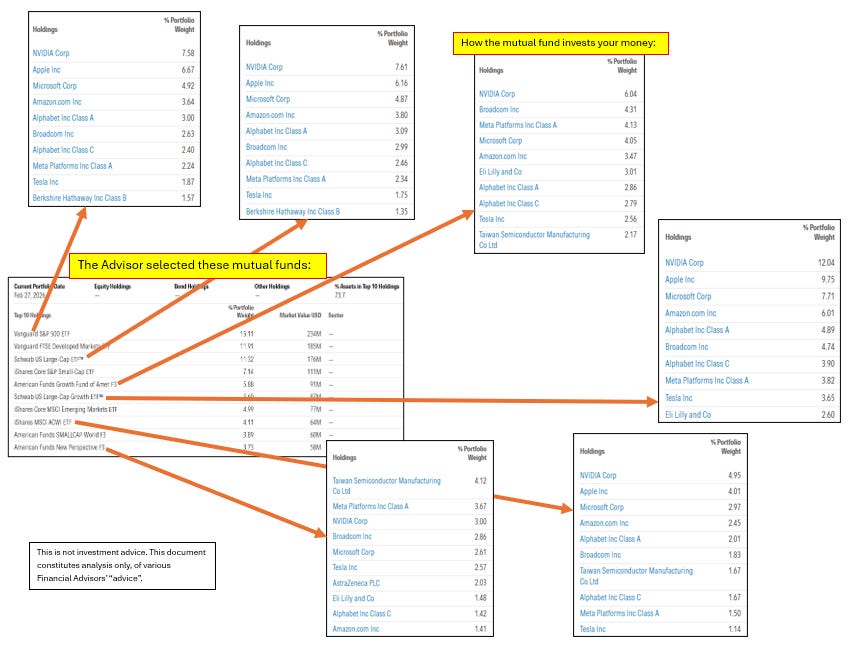

The center box is the mutual funds they’re choosing to use. The boxes at the end of the arrows are the top 10 investments in six of the ten funds. Are they doing a good job of avoiding highly inflated stock prices and helping savers to diversify their investments? Are they avoiding duplicating your investments (the term for this is “portfolio overlap.”)

Unfortunately, the Advisors behind this offering are very large and have a lot of name recognition. They report managing around $260 Billion of investors’ savings, which means that a lot of people will trust them, and many are unlikely to be aware of the fees being siphoned out of their accounts. It’s difficult to say how much of that might be subject so such high fees and woke-Left duplicate funding, but this initial deep-dive doesn’t speak well for due diligence.

Better answer:

Eliminate all those fees. We talk about this often on UnWoke.Academy, like our “behind the veil” 401(k) episodes. Add SDBA and ditch both Plan Advisor and Fund Management fees. Avoid traps trendy traps like paying opaque fees for mismanagement.